They’re not even subtle about it. The system directly rewards you for being in enough debt to always be paying someone interest but not enough that you might file for bankruptcy.

You don’t have to be in debt, but you do need open credit lines. Having debt on them actually makes your score worse.

Her score likely went down because she closed out a credit line, i.e the open loan, so technically the “i have an open 5yr loan ive been paying on diligently” is no longer part of her score. The fact that she did pay it off is part of that score, but its weighted differently.

If she instead had 40k of credit cards she had open for 5yrs, with zero debt on them, her score would have gone up. Just having the account open, even not using them, shows a high “credit to debt usage” ratio and “a long time open loan.” Both of those make up about 45% of your “credit score.”

So no, you dont have to use a CC every month to keep a high credit score. If you want a high score, you want to open a credit card or 2 for their max value until you get about 30k-40k of total credit, and then don’t use them at all. Not a bit. Never close them. The “long time accounts” + “high amount of debt not in use” + “never delinquent” is roughly 80% of your score. You can sail into the 700s/800s if you dont have any other credit hit.

While this is all technically correct it’s still dogshit that your score goes down when you do the thing you are supposed to do with a loan.

Your options are:

Take out a loan and pay it off: score goes down

Take out a loan and don’t pay it off/default: score goes down

They like their little debt slaves

My uhm, social score… cough, I mean credit score is very good right now. I’ve been a good little capitalist.

Credit rating measures your profitability to the credit industry, if you pay off your loan early, they make in interest, thus less profit.

Not entirely true. I’m what they call a deadbeat (meaning I pay off my cards in full every month and have been doing so for the past 10 years, making them $0 profit), and I have a 800 score.

I think the more correct way to think about it is that it’s an estimate of your profit potential. What everyone tells you to do with a score this high is to buy a house because you qualify for the best mortgage interest rates. But of course then they’ll have me on the hook for the next 30 years, and they stand to make in excess of $100k in profit.

100K profit on a mortgage? that’s insane

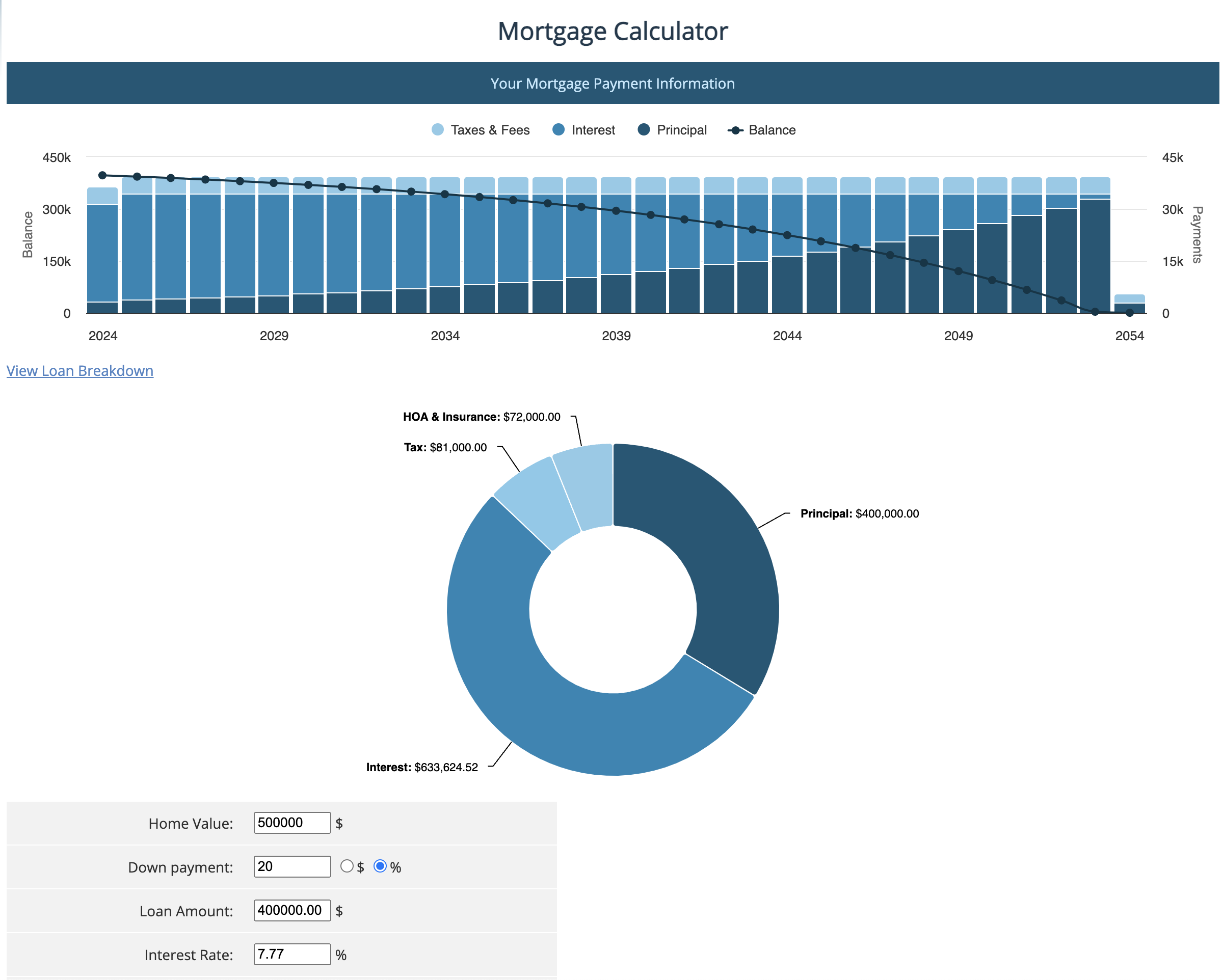

It’s actually far worse than that. If you get $400k loan at the current rate and pay it off over 30 years, you’ll end up paying over 1.5x times the principal in interest. Over the lifetime of the loan, a $500k home will cost you over $1M.

(from mortgagecalculator.org)

Wait why are the banks investing in home loans when instead investing that money into the stock market (should?) yield greater returns over the course of the loan period (even at a very conservative 5% yearly compounding interest, $400,000 turns into $1.7M over the course of 30 years)

Mortgages are fixed income. Stock market returns are variable and therefore riskier. One bad year can wipe out multiple years of gains. Meanwhile, the money you collect as interest has already been paid, and as you can see from the calculator, the interest is front loaded, meaning the majority of it is paid at the beginning of the loan. So even with the probability of a default wiping out the remainder that’s owed, it’s still a much safer investment.

Why aren’t these practices considered criminal?

What is your proposed alternative system? All of this is just an interest rate applied to an outstanding balance. Many less people would own a house without such an option.

I’ll take a lower score and no debt. They can eat their score.

They said, getting an offer for as low as 20% on their mortgage.

I said, having locked in at 2.75 when rates were at a record low.

So the secret to not worrying about credit score is simply already have the loans you want at an interest rate you want. Why didn’t I try that???

I paid a credit card down from $1700 to $1200. My score went from 795 to 763. Fuck 'em and their fake money.

You’re still carrying a balance of $1200 though. Pay it off and it should go up.

There is a lot of misunderstanding about credit scores posted here.

The purpose of credit scores is to answer only one question:

How good are you at pay back a debt if someone were to loan you some money?

Thats it. Everything on how the score is calculated is weights and measures to service that question.

The reason that making payments on an active loan improves your score, is because it is real proof you are getting money from somewhere (the credit score doesn’t care where) and you’re choosing to spend that money on an agreed payment on the debt. Lets say I’m a lender and I’m considering giving you money, and I see that someone prior to me make a similar agreement, and you’re honoring that agreement to pay, then it gives me a good reason to think you’ll also pay on debts you have with me. The reason your score goes down when you pay off your last loan, is because I can’t see you still have the money to pay on a new loan. It means you’re a (slightly) higher risk because I’ll have to take it on faith that where ever you got the money to pay off the last one, you’ll also be able to get that money to pay off the one to me. There’s no guarantee for that, so its a risk to me, a lender.

Another thing I’m seeing missing in the discussion here is:

“Doing X makes your credit score go down”

Technically true, but many of those things that make it go down only do so for a short time. Maybe a month or two (using modern FICO score system).

There can be arguments as to which inputs they use, and how much each of those inputs affects the score. So much so, rating agencies themselves even change their minds over time. They update what they think is important and downgrade what they think matters less. You’ve likely heard of a FICO score. Over time there have been SIXTEEN DIFFERENT VERSIONS of what makes a FICO score source. Some of the variation you see when you get your score from different places is those places using slightly newer or older versions of the scoring system.

Unfortunately lots of organizations that have nothing to do with lending you money are choosing to use your credit score for their own systems. I’ve heard of insurance companies using FICO scores as inputs to how they calculate premiums, which they shouldn’t do. Some employers are using these now to filter applicants. Those employers are perverting the credit score system (again, a system just for loaning money) as a measure of trustworthiness or fidelity. I wouldn’t mind laws that prevent that as that isn’t what credit scores are designed for, and doesn’t answer that question.

How good are you at pay back a debt if someone were to loan you some money?

That’s the point!!!

The only information we are given is that the OP paid off a debt and the credit score went down. You claimed that maybe it is only temporary. But that still goes against your giant text claim.

Why does paying back a debt announce that you are bad at paying back a debt?

I shat my credit into single digit range threeish decades ago (yeah, I’m a boomer puke). I couldn’t even get a bank account until about eight years ago. I finally was able to get an acct, got a secured card, and built my credit up to 729. ‘Upgraded’ my secured card to unsecured, but left the limit at $300 to keep me in check.

Then I made the mistake for applying for a modest credit line with my bank. Not only did I get denied, but the hard credit hit put me under 700. Then my credit took another major hit because I used that card for more than 31% of its limit. Never once made a late payment, neither.

As I hoped that a line of credit could afford me access to an oral surgeon (which I really need to even consider dentures, as I have mucho malo in my mouth), and as I have no interest in writing a grant to cover it, I’m fucked, as oral surgeons don’t seem to take Medicaid in my shit state.

If I survive another yearish, Medicare might be helpful, but the problems in my pie-hole might not wait that long.

I do not want a handout. I want the chance to pay it off and not leave it to Medicare…and not die of the infections spreading to either my brain (such as it is) or my heart.

(Yaay, America!)

Why do you use credit cards in the first place? As a non American I never really understood that. Why doesn’t America just have the “normal” (from my perspective) bank cards that just let you use money from your bank account. Why do you need to borrow and pay back? It seems like such a weird system, not just weird also dangerous, where you can end up in debt.

American here. We have normal cards, they are called debit cards and are what most people use. Generizing a lot here, but credit cards are for people who were never financially educated, desperate poor people, or people who only use them to get plane miles or cash back.

It’s absurd to me to put myself in debt for all but the most desperate of cases.

Thanks, I didn’t know that, you always hear about credit card (debt) but never about debit cards. Can you still use the for a good credit score?

I don’t think debit cards or their associated bank accounts affect your credit in any way since those transactions don’t go through any of the credit agencies.

When I was just starting out in life, I had a credit card but only used it maybe once a year. Just with that I somehow had a credit score in the upper 700s.

Have you considered committing a crime and getting caught so that you can go to prison for a year or two and get free dental?

As much as I can see the appeal of gaming the system, I don’t look good in orange.

Also, I have gigs to attend to (filthy bass player here), as well as taking care of my sweetheart, who has wicked mobility issues. I don’t think I can do that from a cell.

I like the cut of your jib, tho’.

ITT I’m seeing a few common misconceptions repeated by many otherwise correct and knowledgeable commenters without remediation. I’m addressing them here, because understanding financial systems empowers everyone, whether they wish to use them, change them, or burn them to the ground.

- Lenders only see your credit score. Mixed truth. Lenders can order specific scores to get a quick idea of credit-worthiness, but for most credit decisions a credit report or ordered. (This is often called a hard inquiry, and indicates a credit was applied for. A single inquiry is basically ignored by most scoring models. Many inquiries in a short timespan can be considered risky.) Regardless, the report is the same one you see when you order it directly from a credit bureau.

- Your credit score is universal. Mostly false. Credit scores are just someone’s guess of your risk to a lender based on data reported by previous lenders. Good guessers can make money guessing, but none are perfect, and some are only good at guessing risk for specific contexts. Who are they? First, there are the bureaus. They have various branded scores that they sell as products to lenders (for credit decisions) and borrowers (for credit building). Next, there are numerous companies who exclusively develop and sell scoring models. Finally, some lenders such as larger banks develop their own internal scoring models. All the above are adjusted regularly and tailored for specific industries and debt classes. I say “mostly false,” because it’s true that many scores use similar scales and the same records, which means they tend to rise and fall together. That’s why lot of people, even financial wellness advocates, often talk about “your score” as if it’s a single agreed-upon value, but the reality is scores are numerous, distinct, and variable.

- Credit reporting agencies use personal information for scoring. Mixed truth. Many bureaus have affiliated entities that broker financial data for ad revenue, but the information they are allowed to distribute in credit reports is tightly regulated in most countries. (Exceptions: there are alternative scoring model providers who fill a gap of niche debt types sought by applicants with no credit history, such as LexisNexis’ “RiskView” which can use more personal details like address stability and online purchase history to determine risk.)

- Credit history is permanent. False. Negative records like late payment, non-payment, and bankruptcies have expiration dates by law in most countries. Aside from when accounts were opened and closed, generally nothing in a credit report is permanent, and the scores can be extremely variable in practice.

- I should worry about my old credit score. False. Credit scores are used and discarded. New score overwrites old. The only thing that persists would be a credit decision, if there is one. Most scores are partially based on transient data and thus can bounce around wildly. For example, VantageScore 2.0 can dip by over 150 points because a large transaction put a card slightly over the limit but then rebound 150 points after the balance is reported within the limit. Similarly, FICO 8 can jump by 100 points just because the applicant was added as an authorized user to a card with a long payment history. Likewise, most scores can rise and fall drastically based on credit utilization (which is usually reported based previous statement balance, meaning even if you pay off cards every month your credit score will fluctuate in proportion to variance in monthly spending).

- Banks like credit card debt. False True. (Corrected by @d00ery@lemmy.world) Banks love it when you carry a balance. The interest accounts for the majority of their revenue.

The volatility of scoring is the most important takeaway, I think. The temporary nature of scores can be exploited pretty easily. If you understand how they work, you can often get the score you need at a particular time with a bit of planning. And the rest of the time, when you aren’t using your scores for anything, they’re vanity numbers at best.

Anyway, if I missed something or am wrong, please point it out.

I was under the impression that many hard inquiries in a small time frame was ignored because it means you’re shopping for a loan.

Having a single hard enquiry every so often would mean you’re needing to keep borrowing money for some reason.

True. This inquiry collapsing behavior is a feature of recent iterations of two popular models: FICO (8,9,10) and VantageScore (2.0,3.0).

Note however that:

- It only works for certain types of debt. For example, FICO8+ includes auto, student, and mortgage. VantageScore2+ includes utilities, auto, mortgage. No model includes revolving accounts like credit, retail, or charge cards.

- The inquiry collapsing behavior only occurs within a single asset class. For example, FICO8+ would collapse simultaneous shopping for student loans, car loans, and mortgages into 3 inquiries, not 1.

- The shopping period varies. FICO8+ ignores same-class inquiries for 30 days and collapses same-class inquiries within a 45-day window. VantageScore2+ does the same but only within a 14-day window.

Bonus hack: Certain banks also routinely collapse/reuse inquiries for same-day applications, permitting additional applications “for free,” which can be useful if you are denied your first choice and have a fallback in mind or if you are instantly approved for one product and want to try for another.

{kind=link}